Motor Vehicle Repair

Motor Vehicle Repair

This information describes the sales and use tax topics related to the motor vehicle repair industry. Use the links in the Guide Menu to see information about that topic.

Definitions

Definitions

Some of the items and services used to repair motor vehicles are taxable, and some are exempt from sales tax. The taxability of a given item may depend on its exact use, the kind of business providing it, and how parts, materials, and service are broken down on the invoice.

The following definitions apply to this industry.

Taxable Sales

Taxable Sales

Local Sales Tax

Local Sales Tax

Some cities and counties have local sales and use taxes. If you are located in or make sales into an area with a local tax, you may owe local sales and use tax. For more information, see Local Sales and Use Taxes.

To determine the sales tax rate, use the location where the product is received by the customer, typically your business or a delivery address. You can use our Sales Tax Rate Map or Sales Tax Rate Calculator to help you determine the sales tax rate.

Note: The map and rate calculator do not include special local taxes.

For more information, see:

Repair Paint and Repair Materials

Repair Paint and Repair Materials

You may purchase repair paint and repair materials exempt for resale if they:

- Become part of the vehicle

- Are consumed in providing the vehicle repair service

To purchase repair paint or repair materials exempt, give your supplier a completed Form ST3, Certificate of Exemption. Specify the Resale exemption.

Note: If you choose not to purchase repair materials exempt for resale, you can continue to pay tax on the purchase of materials and not charge tax to your customers. See Method 3 in the Handling Sales Tax on Repair Materials section.

Examples of Repair Paint and Repair Materials

| Abrasives | Clear coat | Motor oil | Sealer |

| Acetylene | Degreasing agents | Oxygen | Solder |

| Battery water | Diagnostic dyes | Paint thinner | Solvents |

| Body paint | Glaze | Polishes | Striping tape |

| Body filler/putty | Grease | Primer | Tack cloth |

| Bolts and nuts | Grinding discs | Razor blades | Waxes |

| Brake fluid | Hydraulic jack oil | Sanding discs | Welding rods |

| Buffing pads | Lubricants | Sandpaper | |

| Chamois | Masking tape | Scuff pads |

Note: Service providers must pay sales or use tax on items used to provide repairs on multiple vehicles, such as machinery, tools, and equipment.

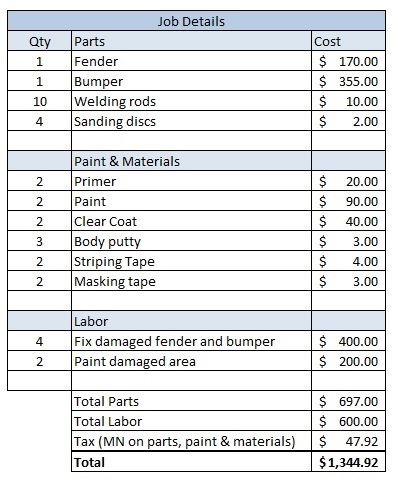

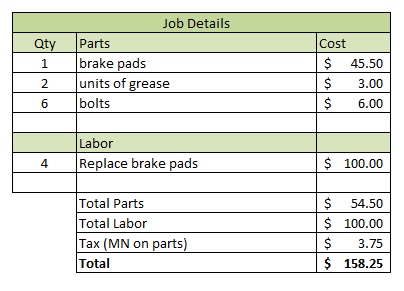

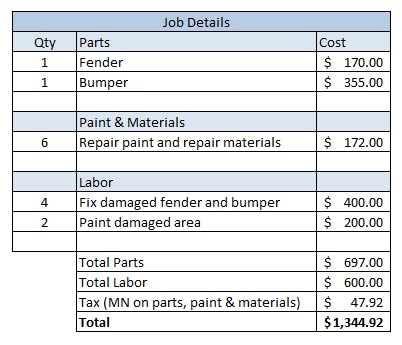

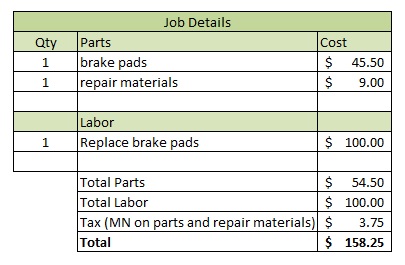

Handling Sales Tax on Repair Paint and Repair Materials

Handling Sales Tax on Repair Paint and Repair Materials

You must handle sales tax on repair paint and repair materials by using one of the following three methods listed. You must remain consistent in the method you choose.

Nontaxable Sales

Nontaxable Sales

Some motor vehicle-related sales are not taxable.

Motor Vehicle Repair Labor

Auto body and mechanical repair labor is not taxable when it is separately stated from repair parts on the invoice.

Custom Painting

Labor charges to custom paint a vehicle are not taxable. But the paint and materials used are taxable. You must either charge sales tax to your customer, or pay sales or use tax when buying these materials.

Tire Recapping and Retreading

Charges to recap or retread a tire are not taxable. These are considered vehicle repair, even if the new cap is of a different tread design (such as snow tread applied over summer tread).

Waste Disposal Fees

Charges for disposing of hazardous waste are not taxable when separately stated on the invoice.

Examples include:

- Antifreeze

- Battery fees

- Special charges for disposing of oil

- Tires

Miscellaneous Sales

Miscellaneous Sales

Sales tax may or may not apply depending on who you're selling products to.

Warranties and Service Contracts

Warranties and Service Contracts

Purchases and Use Tax

Purchases and Use Tax

Legal References and Resources

Legal References and Resources

The legal references and resources related to the motor vehicle repair industry are listed.